Image courtesy of the Mortgage Bankers Association

Mortgage credit availability increased in July according to the Mortgage Credit Availability Index (MCAI), a report from the Mortgage Bankers Association that analyzes data from Ellie Mae’s AllRegs Market Clarity business information tool.

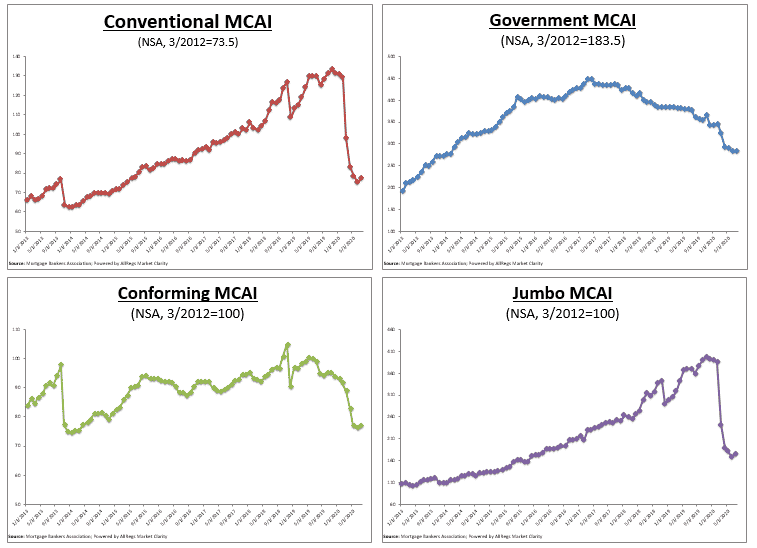

The MCAI rose by 1.5 percent to 126.9 in July. A decline in the MCAI indicates that lending standards are tightening, while increases in the index are indicative of loosening credit. The index was benchmarked to 100 in March 2012. The Conventional MCAI increased 2.9 percent, while the Government MCAI increased by 0.4 percent. Of the component indices of the Conventional MCAI, the Jumbo MCAI increased by 5.0 percent, and the Conforming MCAI rose by 1.2 percent.

“Credit availability rose slightly in July – the first increase in eight months – as the supply of certain types of adjustable rate mortgages (ARMs) and jumbo loans increased. The improvement was more of a leveling off from the precipitous drop earlier this spring. Credit availability is still over 30 percent lower than a year ago and near its lowest level since 2014,” MBA Associate Vice President of Economic and Industry Forecasting Joel Kan said in a statement. “The July data signals that lenders saw conditions improve this summer, as forbearance requests flattened, and record-low mortgage rates spurred strong levels of purchase and refinance activity. There’s evidence the resurgence of COVID-19 cases has cooled the job market recovery, which may temper borrower demand and the overall improvement in the economy.”

The lower availability of mortgage credit – caused by lenders pulling back in the face of uncertainty caused by the coronavirus pandemic – has caused some to worry the residential real estate market could suffer despite a summer that’s seen significant surges in buyer interest.

The MCAI rose by 1.5 percent to 126.9 in July. The Conventional MCAI increased 2.9 percent, while the Government MCAI increased by 0.4 percent. Of the component indices of the Conventional MCAI, the Jumbo MCAI increased by 5.0 percent, and the Conforming MCAI rose by 1.2 percent.

The Conventional, Government, Conforming, and Jumbo MCAIs are constructed using the same methodology as the Total MCAI and are designed to show relative credit risk/availability for their respective index. The primary difference between the total MCAI and the Component Indices are the population of loan programs which they examine. The Government MCAI examines FHA/VA/USDA loan programs, while the Conventional MCAI examines non-government loan programs. The Jumbo and Conforming MCAIs are a subset of the conventional MCAI and do not include FHA, VA, or USDA loan offerings. The Jumbo MCAI examines conventional programs outside conforming loan limits, while the Conforming MCAI examines conventional loan programs that fall under conforming loan limits.